Exercising Stock Options - Don't Leave Money on the Table

May 28, 2021

Startup Employee Series (Part 3 of 3)

When exercising stock options, planning ahead will allow you to capture as much upside potential as possible.

Recap – Part 1: “triple-pain” in down markets:

- Employment status inherently less stable

- Losses suffered in retirement “savings” (qualified retirement) plan

- No control or access to “savings” when it is needed

Recap – Part 2: employee stock options are not really a bonus:

- Even if you perform, the value of the “bonus” is not guaranteed

- You must first buy your participation in the “bonus”

- Significant stock option upside can be thrown out the window if exercised inefficiently

Part 3: Leaving Money on the Table

In this article, Part 3, we will focus on the lost upside financial gain most startup employees experience when exercising stock options. The underlying stock appreciates but the employee uses a “cashless exercise.”

If you took on the risk to work at a startup company, does it make sense to give up a portion of the financial upside you were granted as compensation for that risk?

Here is the gist:

In the event that your underlying stock appreciates in value, you must have cash to efficiently exercise your options or you will lose out on (potentially significant) upside appreciation of your owned stock due to share liquidation, higher taxes, or both.

The Basics of Exercising Stock Options

In order to understand the concepts below, if you are not already, you will need to familiarize yourself with the basics of exercising your stock options and the tax implications. Below is a brief overview.

In this article, we are going to focus on “non-qualified” employee stock options (as opposed to “qualified” (or “incentive”) options).

What is actually happening when you exercise your employee stock options?

Exercising your employee stock options is the process in which you “exercise” your right to buy the underlying company stock:

1. Cash Exercise – A cash exercise is when the options are purchased with cash. With a cash exercise you come out of pocket for the cash required to buy your options at the exercise price (the price at which you were granted the options).

Example: if you have 1,000 options at an exercise price of $10, in order to buy all of your shares, you would pay $10,000 in cash.

2. Cashless Exercise – A cashless exercise is when shares are purchased on your behalf at the (presumably) lower exercise price. Then, a number of shares are immediately liquidated at the (presumably) higher current price to cover the cost of purchasing the shares (plus any broker fees, if any). With a cashless exercise, you do not come out of pocket any money to buy your shares, but you end up with fewer shares at the end.

Example: if you have 1,000 options at an exercise price of $10 and the current price of the underlying stock is $50, you would liquidate 200 shares at $50/share to cover the $10,000 exercise price of the options. At the end you would own 800 shares (1,000 – 200).

3. Tax on Additional “Compensation” – Regardless of cash vs. cashless, taxes will also be due when you exercise options. In the above examples 1,000 shares were purchased by exercising employee stock options. The exercise price was $10/share and the current value of the stock was $50/share. That $40/share increase in value is called the “bargain element” and is considered additional compensation. As such it is taxed as ordinary income.

Example: 1,000 shares x $40 = $40,000 in additional compensation. 24% tax = $9,600 in tax incurred at exercise. The total cost to exercise your shares is $19,600 ($10,000 to buy shares + $9,600 in tax).

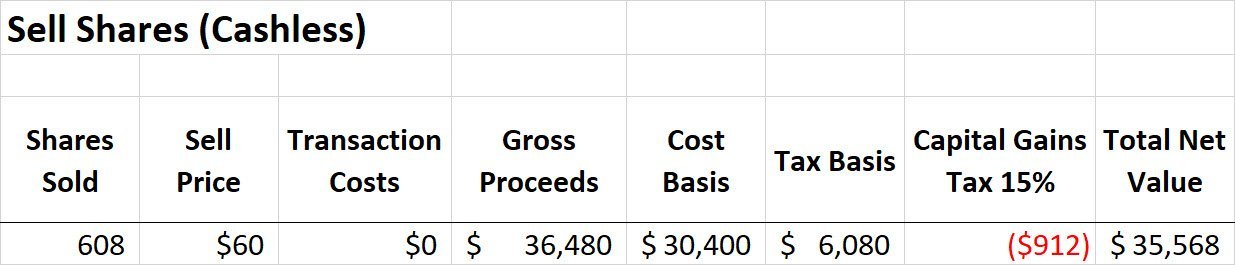

In a cash exercise, this tax cost is paid in cash. In a cashless exercise, additional shares are liquidated to pay the tax. At $50/share, an additional 192 shares would be sold to pay the compensation tax incurred at exercise. So at the end of a cashless exercise, you would end up with 1,000 – 200 (to exercise) – 192 (to pay tax) = 608 shares

4. Early Exercise – Early exercise is a type of cash exercise, for all intents and purposes. Early exercise is not always offered, but when it is, it is a very efficient way to exercise non qualified employee stock options. With an early exercise, you are given the opportunity to buy your shares before they vest and often while your company still has the same valuation. Since the company has the same valuation, the shares of stock have not increased in value at the time of exercise – so there is no compensation tax incurred at the time of exercise.

Example: you early-exercise your options to buy 1,000 shares at the exercise price of $10/share. The current share price is still $10/share. Thus there is no bargain element and no compensation tax incurred. Your only cost is the cost to buy the shares at $10/share – $10,000.

HOWEVER – since your shares have not vested nor increased in value, you cannot perform a cashless exercise (i.e., liquidate shares) to cover the cost of buying the shares.

Exercise Overview:

Options for your Options

Of the above exercise strategies, the cashless exercise is, in my experience, the most common way of exercising employee stock options. More often than not, employees take the path of least resistance and just let their HR department handle the stock option exercise. While there are certainly real-world scenarios where a cashless exercise makes the most sense, I think it is important to understand what you might be giving up by sitting in the passenger seat of your stock option exercise.

What, exactly, is being “left on the table?”

As previously described, when options are exercised using a cashless exercise, what is left on the table are the number of shares you are left owning. Often, startup employees are told that you come out even either way you exercise your options (cash vs. cashless). And it’s certainly easier to perform a cashless exercise — your HR department handles all the legwork for you.

Leaving out the cost of money for now – it is true, at the time of exercise, there is no immediate advantage of a cash vs. cashless exercise.

However, this is obviously not the end of the story. You now own the shares of stock. What next?

If you used a cashless exercise, you now own 608 shares at $50/share

If you used a cash exercise, you now own 1,000 shares at $50/share

The rest of the story is what happens in the next year (or more). You may decide to hold the stock so as to take advantage of lower long-term capital gains tax when you sell it.

If that is the case, what does it look like in both scenarios if the stock price goes up from $50 to $60/share?

Cashless Exercise:

Cash Exercise:

To evaluate the cash exercise correctly, we must factor in the cost of money and pay back the source of funding (even if it’s ourselves!) at a reasonable rate of interest, we’ll say 5%.

As you can see there is a 6.6% net increase in value using a cash exercise.

In the below chart, you can see what happens as the stock price goes up. At a stock price of $70/share there is a 14% increase in net value, at $90/share there is a 24% increase, and so on.

This is the money left on the table when you give up shares using a cashless exercise.

Risk

Even though the possible upside is significantly higher using a cash exercise, you are also potentially taking on more risk. If the stock price goes down, that leverage works against you! You can lose the cash you put in.

As previously mentioned, it may very well make sense to look at other strategies than a cash exercise. There may be too much uncertainty around the future of the company and stock value. Using a cashless exercise is a great way to minimize the risks as you are not putting your own cash into the deal.

Some other methods to get cash out of your options and reduce risk might be a secondary option sale or a non-recourse stock option loan. However, with both of these methods, you are still giving up some or all of the potential upside of the stock.

Bankrolling Your Upside

Since we can’t predict the future, ask yourself this question:

Is it better to have cash and not need it -or- need cash and not have it?

Because of the almost-zero earnings on cash, most people are reluctant to keep a lot of it around. This has pushed the average investor into putting their money into riskier stock market-based investments, including the qualified retirement “savings” plan.

There are tried-and-true saving strategies, using specialized cash accounts, such as whole life insurance, that allow you to save for retirement, earn very respectable interest, and still have access to your money.

Because of the tax-advantaged status of these cash accounts, you can build a better, more flexible, and “portable” retirement fund and still have access to your cash. This allows you to take full advantage of any opportunities that come your way, and require cash. You can do this without sacrificing or having to choose between your retirement fund and being liquid with cash.

Whole Life Insurance

It’s like a Savings Account and a ROTH IRA Had a Baby…

If you could have a ROTH IRA but with no income qualification requirements, no practical limits on contributions, no rules about when and how you use your money, no market risk, and full liquidity — how much money would you put into it?

Cash value whole life insurance has been around in the United States for over 150 years and has been used by some of our greatest entrepreneurs to provide liquidity for growing their businesses. People like Walt Disney, JC Penney, and Ray Kroc (founder of McDonalds).

Big Banks are some of the largest life insurance policy holders. Do some research on Bank Owned Life Insurance (BOLI) and you’ll see cash value whole life insurance is held in great amounts as Tier 1 capital on many banks’ balance sheets.

However, you don’t have to be a bank or a titan of business to have one of these cash accounts. Anyone can set them up.

To learn more about why I think whole life insurance could be the best financial asset a startup employee could ever own, see my one-page primer on whole life insurance.